- ian@etherintroductions.com

- 07795 275934

Insurance Supply Chain Experts

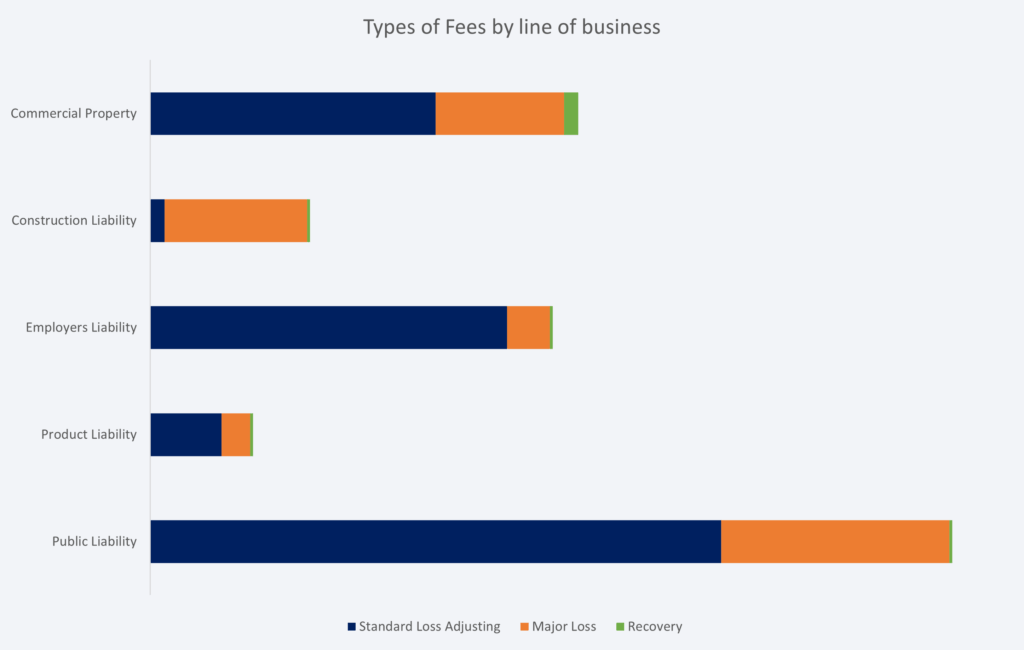

Starting with the basics – comparing different firms fees. This is done by lines of business and then applied by:

The key with banded rates is to understand where your typical claims settlement sits. This way you can compare the band(s) that are most frequent to your book.

We have multiple data sets and are able to advise on how competitive, or not, your negotiated fees are.

Comparing fees by bandings only shows a part of the picture.

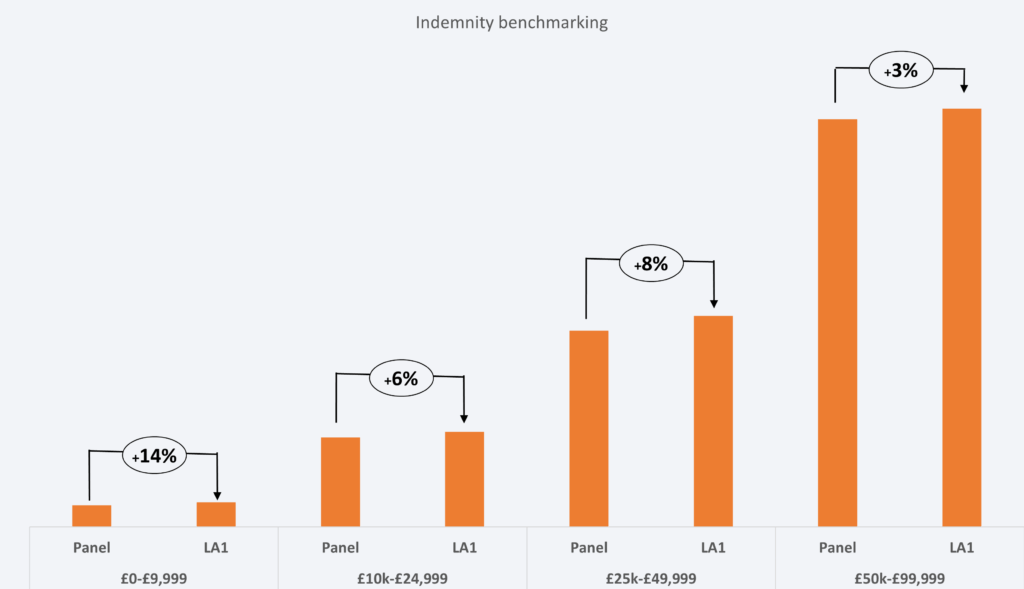

Having undertaken an in depth audit for a leading UK insurer, we found that there was a large difference in average fees. This was despite their being very similar commercial terms.

Firm LA1 was consistently billing more per settlement banding than the other panel firms. In the lower band (up to £10,000) there was no real disparity. In the two bands up to £50,000 however, there was a marked increase in fees.

Our findings showed that on lower value claims, most loss adjuster invoices were as per the fixed fees. At the next two bandings, LA1 was frequently requesting an hourly rate to be applied. This took the claim outside of the pre-agreed fixed fee. This made the average fee significantly higher than the panel average.

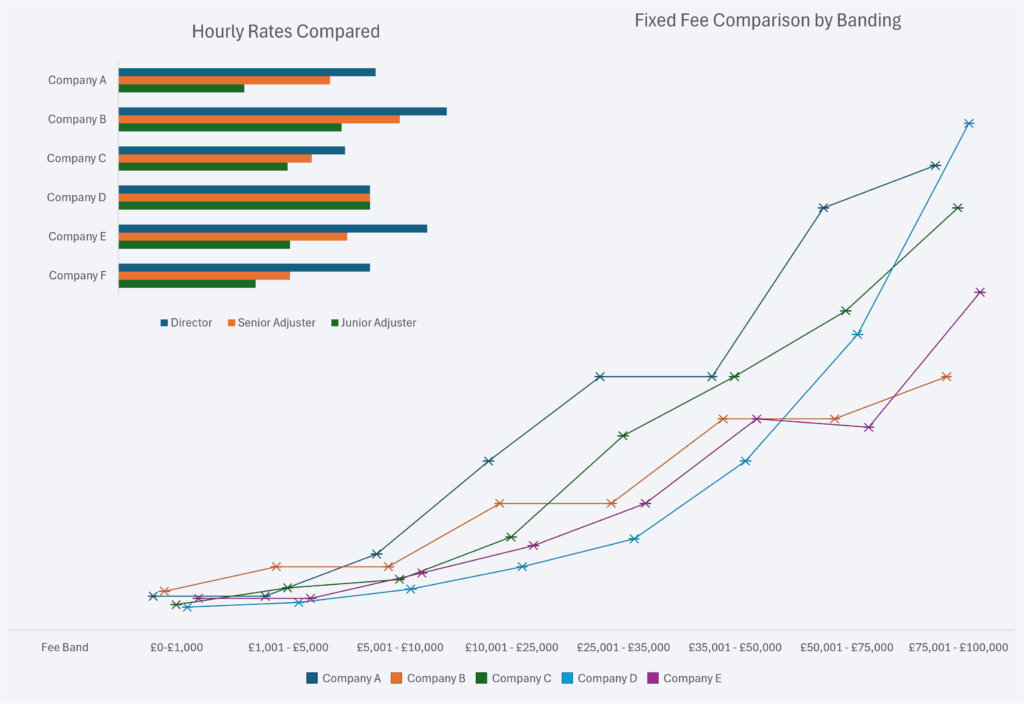

Service costs will naturally vary by line of business so it is vital when comparing average fees or total spend to do this by type.

For example, in a London market audit it was initially felt that the average fee claim settled was too high on Construction Liability claims. However, a data audit soon identified that the vast majority of claims required a major loss adjuster and therefore the application of hourly rates pushed up the average costs.

Conversely, commercial property average fees were the lowest as more claims were billed at the fixed fee bandings and at a recovery rate.

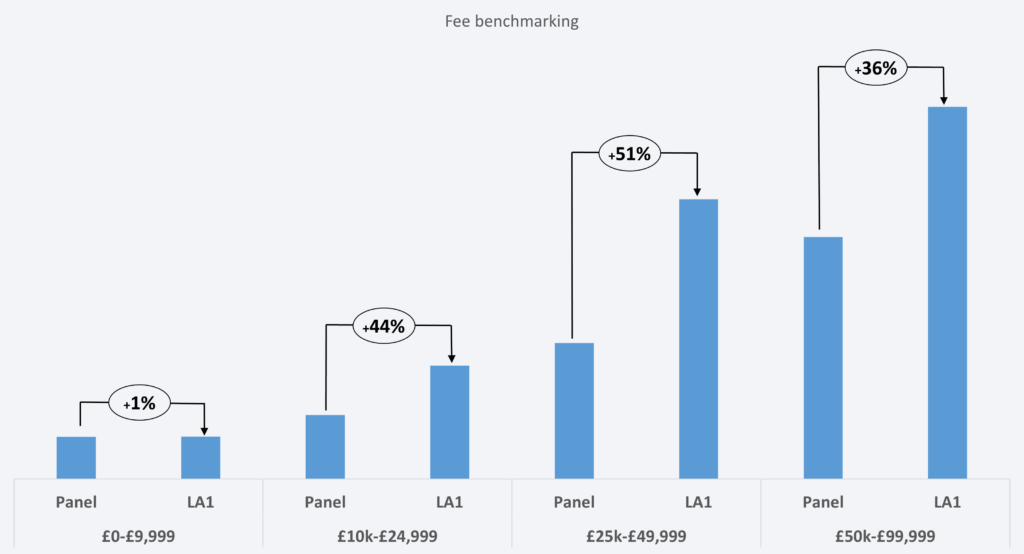

Fees are important but the biggest impact on the claims book is always going to be the indemnity spend. In the case of Loss Adjuster led claims it is ensuring that the panel firm is able to control costs in line with the policy terms and conditions.

In the case of firm LA1, when our audit showed their costs were higher than the panel average, they counter claimed that because of the quality of service, it still represented value for money.

Unfortunately when reviewing the claims outcomes, it became very clear that in fact the opposite was the case and the higher fee was matched by higher average settlement costs.