- ian@etherintroductions.com

- 07795 275934

Insurance Supply Chain Experts

My journey in the insurance industry began as a graduate trainee loss adjuster, handling a wide array of domestic and commercial claims across East London. This foundational experience provided me with a granular understanding of the claims process from the ground up.

Over time, I transitioned into overseeing claims teams and building repair networks, culminating in a leadership role with responsibility for the claims supply chain at a global insurer. I have extensive experience in claims auditing and TPA (Third Party Administrator) management, including the creation and optimization of TPA models suited to Lloyd’s and the broader London market. My skillset includes negotiating legal services in the London market to deliver optimal value and results across complex, multi-jurisdictional claims. This unique career trajectory has given me a comprehensive, 360-degree perspective on the claims ecosystem—understanding not only claims management but also the intricate network of suppliers, partners, TPAs, and technologies that drive successful outcomes across the London insurance market. My expertise enables me to deliver tailored solutions and strategic value for Lloyd’s syndicates and London market participants operating in an evolving risk environment.

I don’t just understand claims; I understand the intricate network of suppliers, partners, and technologies that drive successful outcomes across multiple classes of business.

My experience spans the full spectrum of the insurance claims landscape.

Proud to have consulted for some of the biggest names in the insurance sector.

Let’s discuss how my experience can deliver value to your business. Whether you need strategic advice, project management, or procurement expertise, I’m here to help.

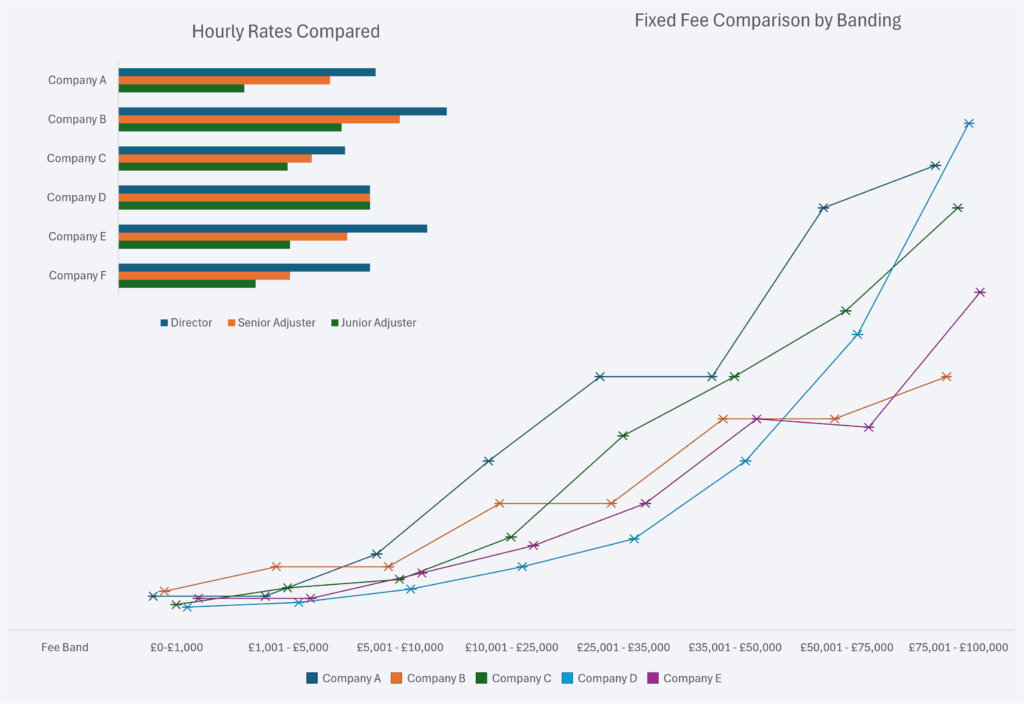

Starting with the basics – comparing different firms fees. This is done by lines of business and then applied by:

The key with banded rates is to understand where your typical claims settlement sits. This way you can compare the band(s) that are most frequent to your book.

We have multiple data sets and are able to advise on how competitive, or not, your negotiated fees are.

Comparing fees by bandings only shows a part of the picture.

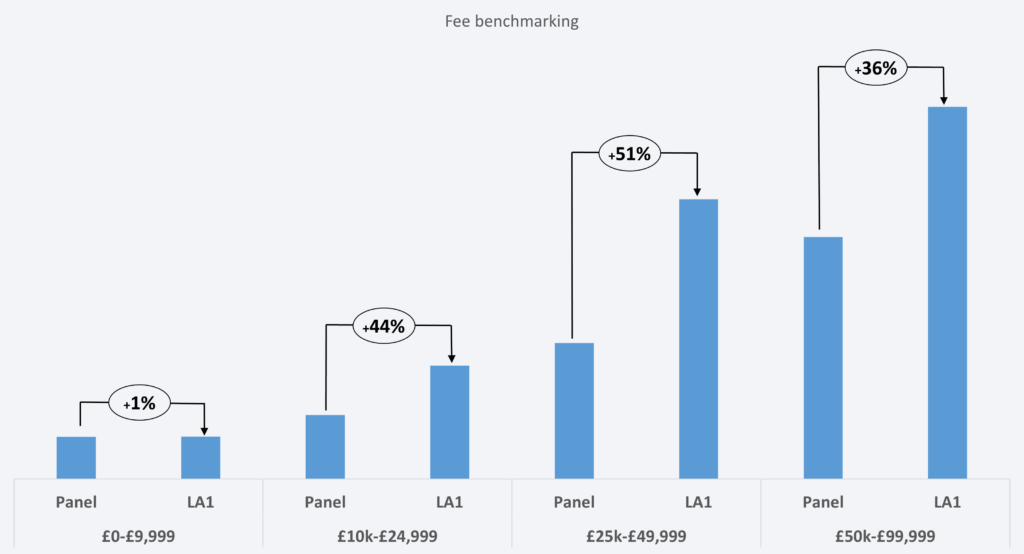

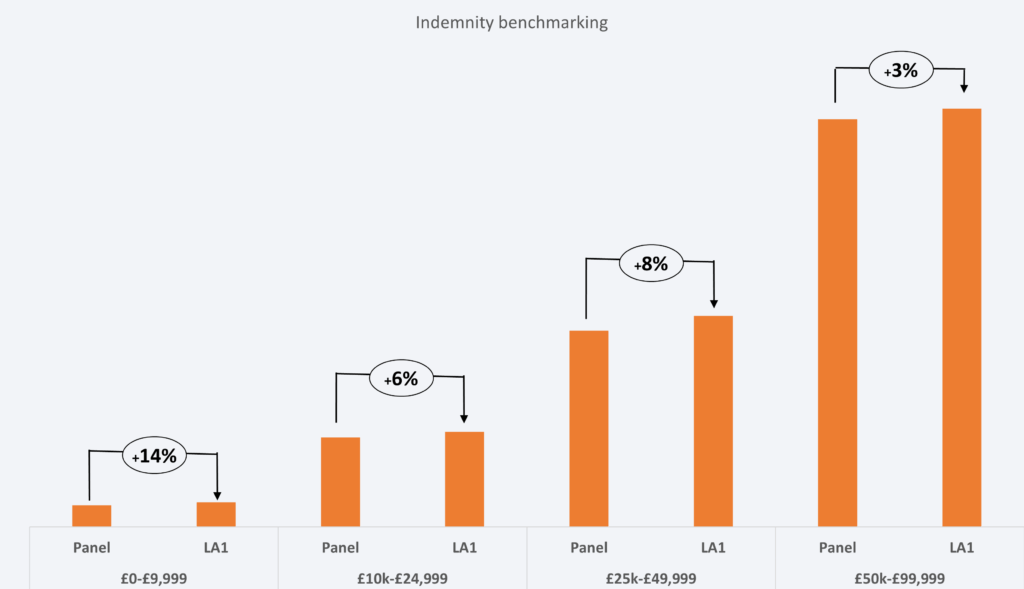

Having undertaken an in depth audit for a leading UK insurer, we found that there was a large difference in average fees. This was despite their being very similar commercial terms.

Firm LA1 was consistently billing more per settlement banding than the other panel firms. In the lower band (up to £10,000) there was no real disparity. In the two bands up to £50,000 however, there was a marked increase in fees.

Our findings showed that on lower value claims, most loss adjuster invoices were as per the fixed fees. At the next two bandings, LA1 was frequently requesting an hourly rate to be applied. This took the claim outside of the pre-agreed fixed fee. This made the average fee significantly higher than the panel average.

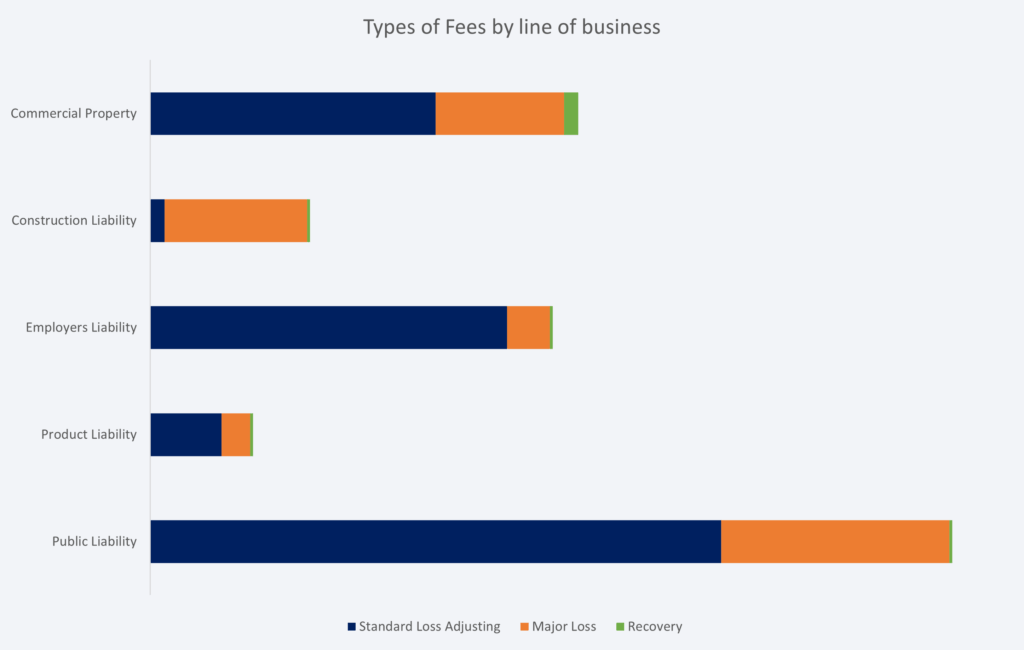

Service costs will naturally vary by line of business so it is vital when comparing average fees or total spend to do this by type.

For example, in a London market audit it was initially felt that the average fee claim settled was too high on Construction Liability claims. However, a data audit soon identified that the vast majority of claims required a major loss adjuster and therefore the application of hourly rates pushed up the average costs.

Conversely, commercial property average fees were the lowest as more claims were billed at the fixed fee bandings and at a recovery rate.

Fees are important but the biggest impact on the claims book is always going to be the indemnity spend. In the case of Loss Adjuster led claims it is ensuring that the panel firm is able to control costs in line with the policy terms and conditions.

In the case of firm LA1, when our audit showed their costs were higher than the panel average, they counter claimed that because of the quality of service, it still represented value for money.

Unfortunately when reviewing the claims outcomes, it became very clear that in fact the opposite was the case and the higher fee was matched by higher average settlement costs.

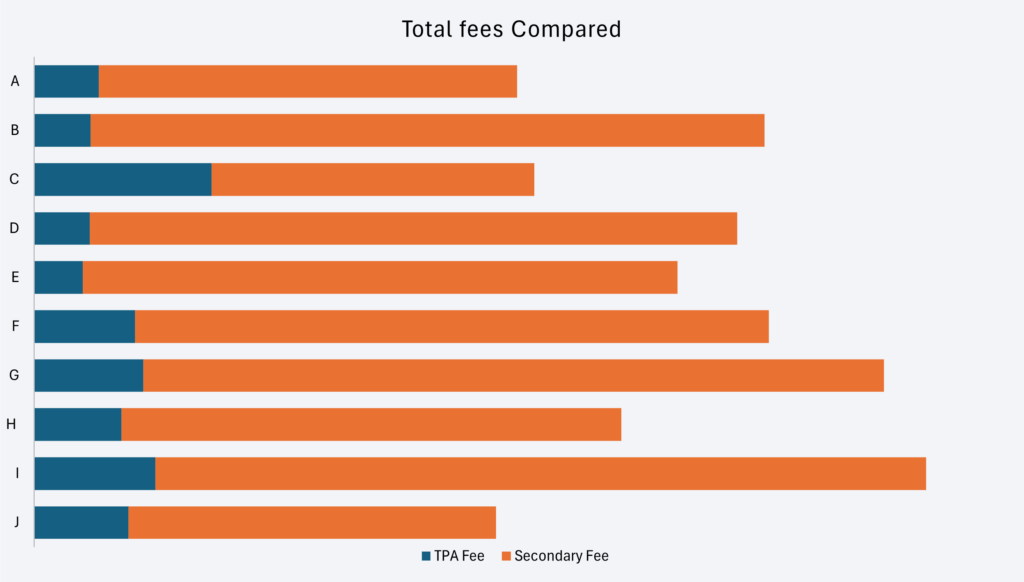

We generally find that TPA fees don’t self-fund; they won’t cover operational costs. As a consequence, the TPA function becomes a loss leader which can only operate at the fee levels they do if that function can feed another part of the business.

For example, we reviewed the TPA panel for a leading London syndicate’s US property book and found the following;

Taking 10 sets of TPA data which cover comparable lines of business, we can see that the secondary fee (loss adjuster or other owned service) is substantially more than the total TPA fee on its own.

Whilst a higher TPA fee can (Firm C) offset the need for higher secondary fees, that is not always the case (Firm I).

The key, as ever, is to be able to compare all aspects of associated fees to be able to provide accurate benchmark comparisons of costs.

Undertaking a full audit of a UK based TPA for a major insurance client, we soon discovered that their primary focus was revenue generation into the wider group.

On average, they were instructing their own companies 2.3 times for each TPA instruction they received. On a large number of instructions, up to 5 group companies were instructed.

The number of low value claims settled at desktop was minimal and secondary fees were spiralling out of control. As can be seen, the TPA fee element of total costs looked quite insignificant.

Fees are obviously only a small part of the overall claims spend. Indemnity, at least on most claims, will always be the higher proportion of total claims costs.

What we look for here is value for money. Larger claims incur larger fees, as do more complex claims even at a lower claims amount threshold.

So when we compare the total fees as a percentage of total claims costs (all fees + indemnity) we can start to draw comparisons between different TPA performances.

On the face of it, Firm E is providing good value for money, whereas Firm G really is not. There is of course a very important caveat to this assumption. If leakage is rampant then value for money will significantly drop. Equally, Firm J looks to be adding less value, but was achieving very strong indemnity controls and fraud detection rates.

It is not just about costs, but service too. When TPA’s instruct themselves it adds complexity and time delays to the claims duration.

Looking at a simplistic measure of indemnity spend vs elapsed days, it is evident that Firm H is taking too long to settle low value claims. In contrast Firms A and G are concluding claims in half that time.

Elapsed days are only one customer measure, but it is an important one.

Managing claims supply spend effectively is crucial. But before you can optimize, you need to

We have full data sets covering the fees incurred, the claims outcome (fulfilled, cashed, zero settlement) and the final indemnity spend for surveyors.

For building repairs we have regional indemnity averages, national indemnity averages and claims management fees comparisons.

At our disposal is a full set of fee data covering various claims types at every value banding.

Of course fees are only one aspect of a loss adjusters output and we have adherence to fee scale data as well as the all important average indemnity controls.

Covering UK, USA and some other territories, we have an extensive data set on TPA’s.

Fees, conversions to Loss Adjusters, indemnity controls and claims outcomes are all covered. We also have data on low value claims as well as more complex and specialist claims.

Over the years we have built up a comprehensive set of legal rates covering most territories around the globe.

These are split by individual hourly rates according to seniority, by type of matter, and by the location the services would be provided.

Multiple data points covering the key metrics which provide valuable insights into how an insurance book of business is performing.

Our insights cover loss ratios, elapsed days from FNOL to closure, reopening rates, claims outcomes, average and total indemnity spend.

From being a loss adjuster out in the field we’ve moved to managing teams and then entire loss adjusting panels. We have extensive data on fee bandings, outcomes and indemnity spend.

We are able to audit panel performance on a case by case basis, covering technical application as well as commercial considerations.

We also have a tried and tested methodology for getting the best performance out of loss adjusting firms.

Having previously run repair networks on behalf of insurer clients this has given us a real hands-on knowledge of how to build a repair strategy for insurers.

We have in depth experience of the eco system of building repairs, covering drying, surveying, restoration, asbestos and restoration. We have set insurer strategies and deployed best of breed solutions.

Either as a stand alone product, a bolt on to a main domestic policy or as a value added cover to the main terms, we have expensive experience in undertaken market reviews of home emergency propositions.

We have previously run multiple audits on performance and then strategic reviews of insurers home emergency propositions.

Having previously worked for contents providers we are uniquely placed to provide insight and strategy for insurers when it comes to contents spend.

We have created and delivered strategies for multiple clients for their contents spend. Primarily we focus on validation, repair and then replacement solutions in order to manage indemnity spend.

Main contents items are flooring, jewellery electrical goods and bikes.

In addition to the main commodities, a complete property supply chain requires a lot more additional services. We have led strategies and tenders for all of them.

Suppliers will typically cover the following;

Glazing services, alternative accommodation, drainage solutions, asbestos testing and removal, garden items, DIY kit, weather validation and prediction services, fraud detection and forensics.